Meet David and Elena

While earning over $300,000 anually combined, David and Elena, found themselves overwhelmed by the complexity of simultaneous life milestones; welcoming a new daughter and preparing to purchase a larger family home.

They wanted to know if their current financial trajectory would allow them to secure a sound present, future and early retirement.

Specifically, they looked for advice on where to allocate their free cash flow; whether to a TFSA, RRSP, or real estate, and sought an unbiased assessment of their investment strategy.

To protect the privacy of our clients, representative stock photography has been used

The challenge: major life transitions

QUESTIONS THEY HAVE

-

How much can we comfortably spend on a new house without risking our future?

-

What is the best way to save for our daughter’s education?

-

How do we plan tax-efficiently to maximize our assets? Should we prioritize the RRSP or TFSA?

-

Are all of our potential financial needs and risks covered?

-

How do we build and maintain a proper emergency fund?

PERSONAL ASSETS

The PLAN

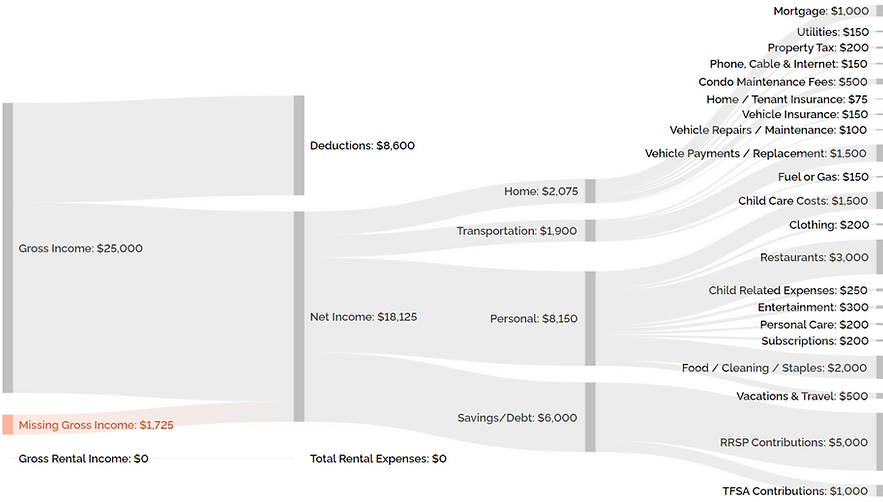

1. CASH FLOW

A cornerstone of effective financial planning is absolute clarity on where your money is going.

We helped David and Elena move beyond "guessing" by identifying exactly where the household's monthly income was being allocated.

Through this process, we determined the household’s free cash flow; the surplus income available after all expenses are met. For many clients, seeing this detailed financial picture for the first time is an eye-opening and empowering experience.

By establishing a clear spending plan, we were able to determine David and Elena's current savings rate, which is the most critical metric for their long-term financial health.

This allowed us to stress-test their ability to handle current market interest rates, providing the clarity they needed to move forward with a $1,550,000 home purchase confidently.

-

Gross Monthly Income: $25,000

-

Net Disposable Income: $18,125 after tax and deductions

Household Surplus

We identified a significant annual surplus to be redirected toward long-term goals.

2. SPENDING

How will their spending change as we approach and enter retirement?

Our analysis confirms that David and Elena's household maintains a healthy surplus cash flow each year leading up to retirement; a vital indicator of their ability to build long-term wealth.

As we look ahead to their retirement years, we anticipate a significant shift in their financial landscape. During this phase, their spending rate typically drops substantially as they transition from saving to decumulation (drawing from their assets).

By this time, major expenses like debt payments are often eliminated and children have moved out, allowing their retirement income to go much further.

Understanding this transition is essential for creating a dependable plan that ensures David and Elena never outlive their money.

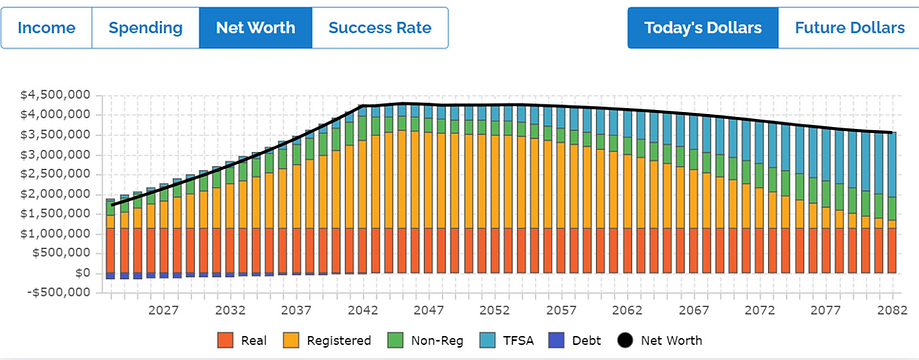

3. NET WORTH

Our analysis shows that a high household savings rate, when allocated and invested professionally, results in a steady increase in your net worth.

Upon reaching retirement, a large asset base combined with modest spending, allows for a gradual drawdown of assets. This strategy ensures David and Elena can fulfill their wishes of leaving a substantial legacy to their children.

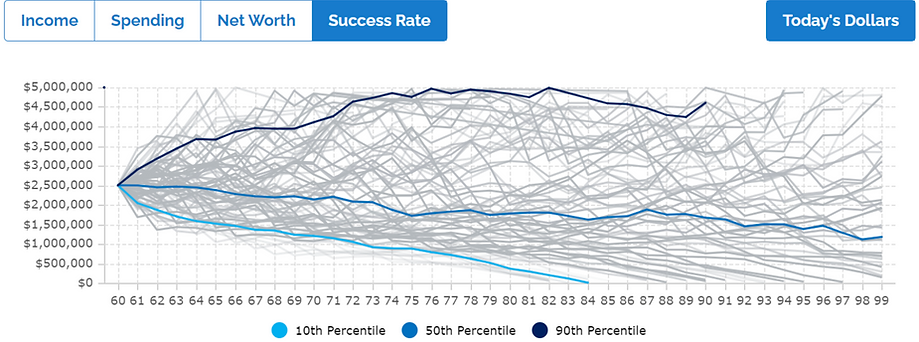

4. SUCESS RATE

Our planning software runs a variety of simulations to determine their plan's success rate and establish a comfortable margin of safety.

We discuss these results openly with David and Elena, making adjustments as needed to ensure the strategy remains aligned with their goals.

5. RECOMMENDATIONS

-

Maximize Education Savings: Start an RESP immediately for David and Elena's daughter. Contribute $2,500 annually to secure the maximum Canada Education Savings Grant (CESG), adding extra funds when possible to claim unused grants from previous years. We also provided a review of the most effective investment options.

-

Home Purchase & Stress Testing: Proceed with the $1,550,000 home purchase. After stress-testing their ability to manage current interest rates for both the new home and their future condo (pre-construction), we reviewed the tax and cash flow implications of selling the pre-construction unit.

-

Asset Diversification & DIY Support: With wealth currently concentrated in real estate and one company’s stock, diversification is essential. As David transitions to DIY investing, we provided best-practice reviews and committed to the ongoing assistance necessary for new investors.

-

Strategic Cash Flow Planning: We established a detailed plan to allocate surplus income toward early mortgage repayment, TFSAs, and RRSPs. This roadmap ensures their money works efficiently while following their specific lifestyle goals.

-

Risk Management: We provided tailored recommendations for life insurance and disability coverage to ensure the family's financial security is fully protected.

THE RESULT

David and Elena moved into their new home with a detailed roadmap.

They now have a clear cash-flow roadmap that balances strategic mortgage pay-down with tax-sheltered growth.

This gives them the freedom to focus on their family today, with the total confidence that their future needs and their daughters’ education are fully secured.