Meet THE CHEN's

Retiring with Confidence: How a retirement Plan Turned Uncertainty into Security

Raymond and Mei Chen (both age 58) worked hard for decades to build their future. They successfully saved over $3.2 million in total net assets. This includes a $1.2 million home and substantial RRSP and TFSA accounts.

Despite their success, they felt uncertain about the future. They weren't sure if their savings were enough to support their current lifestyle through retirement.

They wanted to see what life would look like if they retired at 65 versus a few years early at 62.

Raymond and Mei also didn't know if they could fulfill a major family goal: helping their children break into the real estate market next year.

To protect the privacy of our clients, representative stock photography has been used

QUESTIONS Raymond and mei HAVE

-

Can we afford to retire at 65, and how much can we safely spend each year? Can we retire earlier, at 62?

-

How much can we safely spend in retirement?

-

Can we afford to give our children a significant financial gift for a home purchase next year without jeopardizing our own future?

-

What are our estate taxes and probate fees likely to be, and how do we minimize them?

-

When should we start taking CPP, OAS, and RRIF payments to be as tax-efficient as possible?

PERSONAL ASSETS

The PLAN

1. CASH FLOW

In retirement, your Net Worth is just a number on a page. Cashflow is what you actually live on. Here is why it is the most important part of the planning process:

For 30 years, Raymond and Mei focused on growing their "pile" of money. In retirement, the challenge flips: they must now systematically take that pile apart. Cashflow planning ensures they are are pulling from the right "buckets" (RRSP vs. TFSA vs. Non-Registered) at the right time to minimize the tax "drag" on their wealth.

Cashflow planning maps out how their income will grow over time, by incorporating indexed sources like CPP and OAS, to ensure their standard of living doesn't erode as prices rise.

2. SPENDING

How will their spending change in their retirement?

Our analysis shows that once Raymond and Mei begin collecting RRIF, CPP, and OAS, their income actually exceeds their needs. This yearly cash flow surplus creates an exciting opportunity. It gives them the 'permission to spend' more on travel today or the peace of mind to leave a larger legacy for their children tomorrow.

By mapping out their future income sources, we identified a consistent cash flow surplus starting at age 71.

Because their mandatory RRIF withdrawals and government benefits exceed their planned expenses, they have built-in financial flexibility. They can safely increase their standard of living without the risk of outliving their money.

3. NET WORTH

The chart below illustrates the Chen's projected net worth over their expected lifetime. This is called the decumulation phase; the critical transition from growing a "pile" of money to strategically taking it apart.

Most people believe there is a "standard" order for spending assets, but the reality is much more complex. Our analysis specifically pinpointed the most tax-efficient sequence for the Chen family:

-

Preserving Tax-Free Growth: By determining which assets to spend first; such as non-registered accounts. We allow their TFSA and RRSP/RRIF "buckets" to continue growing tax-deferred for as long as possible.

-

Avoiding the "Tax Spike": We modeled their income to ensure that mandatory RRIF withdrawals at age 72 don't accidentally push them into a higher tax bracket or trigger an OAS clawback.

-

Legacy Protection: The plan ensures they aren't just spending money, but preserving the maximum amount possible for their children's future estate.

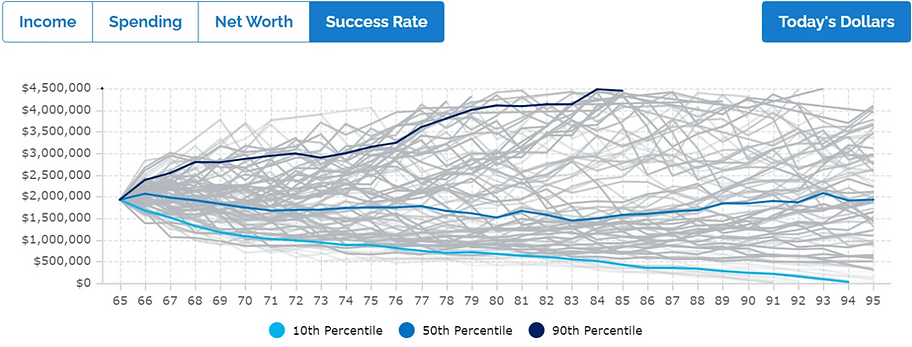

4. SUCESS RATE

Our planning software runs a variety of simulations to determine their plan's success rate and establish a comfortable margin of safety. If the rate is too low, we discuss alternatives to increase success.

We discuss these results openly with Raymond and Mei, making adjustments as needed to ensure the strategy remains aligned with their goals.

5. RECOMMENDATIONS

-

Tested Every Scenario: We confirmed that Mei and Raymond can retire at 65 while maintaining their current lifestyle. Crucially, the plan allows them to give a significant gift to their children next year for a home purchase. While they hoped for age 62, our analysis showed it lacked a sufficient "margin of safety." This honesty gave them the confidence to stick to a plan that actually works.

-

Built a Tax-Smart Income Stream: We optimized their withdrawal strategy to minimize the tax "drag" on their wealth. By drawing from non-registered accounts first and delaying RRIF income, we preserved their tax-sheltered growth. We also implemented income-splitting strategies to ensure they keep more of what they’ve earned.

-

Protected the Family Legacy: Leaving a substantial estate was a top priority. We mapped out the most efficient way to pass on assets while minimizing the "tax bite" at death. We also identified specific strategies to prevent an OAS clawback, ensuring they receive their full government benefits.

-

Optimized the Timeline: We provided a clear "When-to-Start" roadmap for their CPP, OAS, and RRIF payments. Instead of guessing, the Chens now have a month-by-month schedule for their retirement income.

-

Right-Sized the Risk: We conducted a deep-dive review of their existing investments. As they are now in the "retirement red zone," we ensured their portfolio was shifted from pure growth to a more resilient structure suited for their near-retirement situation.

6. The DELIVERY

A financial plan is only as good as its implementation. Our process is designed to bridge the gap between "math" and "real life":

The Discovery Calls

Through a series of focused video consultations, we stress-tested their goals. We didn't just look at their bank accounts; we talked about their values and their desire to help their kids.

The Projections

We provided a year-by-year cash flow roadmap. This removed the guesswork, showing them exactly where their income will come from every single month.

The Action Plan

We concluded with a written, step-by-step report. This isn't a vague document; it is a clear set of instructions; from which accounts to sell first to exactly when to apply for their government benefits.